Micron Up 16%. Apple Down 6%.

Just when you thought AI stocks had run too far to chase, Micron reminds everyone why momentum traders exist.

After reporting earnings on Wednesday evening, Micron (MU) surged nearly 16% on Thursday. Not 16% from some beaten-down base. This was a stock that had already hit an all-time high of $1,134 just days earlier. And it still popped 16%.

Let’s break down what happened.

Shocking Numbers

Micron posted fiscal Q3 2026 revenue of $41.46 billion. That’s not a typo. Just last year in the same quarter, they did $9.3 billion. In other words, revenue more than quadrupled year-over-year.

To put it another way, Micron grew by nearly $18 billion in a single quarter compared to the prior quarter’s $23.86 billion. The beat was across the board. Revenue came in 16% above analyst estimates, and adjusted EPS of $25.11 beat forecasts by over 22%.

Data center revenue hit $25 billion in one quarter, an annualized run rate of over $100 billion. Enterprise SSD revenue alone exceeded $5 billion, more than doubling sequentially.

And if you thought Q3 was good, management’s Q4 guidance was something else entirely.

Analysts expected Q4 revenue of around $43 billion. Micron guided to $50 billion.That’s nearly a $7 billion beat on guidance.

Free cash flow in Q4 is expected to exceed $30 billion. HBM3E and HBM4 are fully booked through calendar 2027, with demand already extending into 2028. They also locked in $22 billion in strategic customer agreements, including $18 billion in upfront cash deposits. Customers are essentially pre-paying to secure memory supply.

When your customers are handing you cash in advance just to get in line, you’re not in a commodity business anymore. You’re controlling supply and dictating prices.

But Wait, Didn’t Micron Just Drop 12%?

Here’s the part that makes this story even more interesting.

Just 48 hours before this blowout results, Micron was down sharply. It was part of a brutal semiconductor selloff on June 23 tied to AI valuation fears and a crisis in South Korean leveraged ETFs tracking memory chip peers. Sandisk fell 12.5% that same day. The mood was ugly.

And then earnings hit.

That’s the brutal reality of momentum trading in AI stocks. One day you’re down 12%, the next you’re up 16%. The swings are violent in both directions, and only those with the stomach and the discipline can ride them.

Micron’s results didn’t just move Micron. They sent a wave through the entire semiconductor ecosystem.

SanDisk (SNDK) surged over 20%, building on its position as the top-performing S&P 500 stock of 2026 with a staggering 748% year-to-date return. The logic is straightforward. If Micron’s NAND and HBM supply is fully booked, the same shortage is lifting SanDisk’s pricing power.

The rest of the AI value chain were up too. Applied Materials (AMAT) rose around 13% after launching six new chipmaking systems designed for DRAM production and advanced AI chip packaging. More Micron orders means more machines needed to make the chips. Teradyne (TER) and Corning (GLW) also had strong days, up around 10 to 11% respectively. You might wonder what a fiber optics company like Corning has to do with memory chips. The answer is that as AI data centers scale, everything around them scales with it, from testing equipment to optical connectivity. These are the picks-and-shovels plays of the AI build-out.

Micron’s Gain Is Apple’s Pain

The same memory shortage that’s minting money for Micron is creating a serious headache for Apple (AAPL).

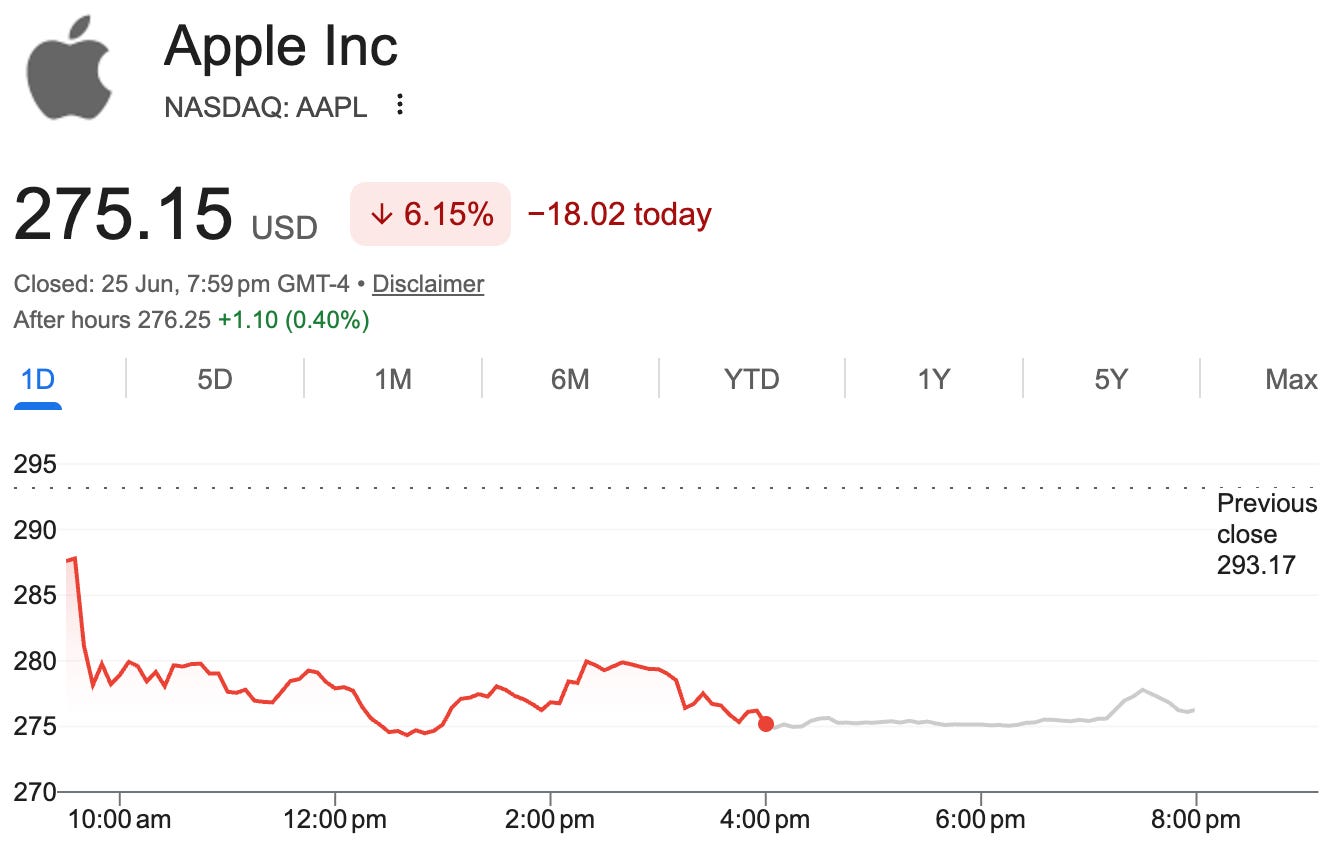

On Thursday, Apple announced price hikes across its MacBook and iPad lineups. The MacBook Air jumped from $1,099 to $1,299. The MacBook Pro 14-inch went from $1,699 to $1,999. The iPad Air rose from $599 to $749. CEO Tim Cook described the memory supply squeeze as a “hundred-year flood,” with DRAM and NAND prices surging as the entire industry prioritises AI data centre chips over consumer electronics.

Apple’s stock fell over 6% on the day, its worst single-day drop since April 2025.

This illustrates a zero-sum dynamic playing out in real time. The AI infrastructure boom is diverting semiconductor supply away from consumer devices. What fills Micron’s order books reduces Apple’s margin.

And it’s not just Apple.

The MAGS ETF, tracking the Magnificent Seven, fell about 6% over the past week.

The hyperscalers and AI capex spenders, Microsoft, Google, Amazon, Meta, have all seen their share prices drift lower about 6% this week. The market is effectively penalising the buyers of AI infrastructure while rewarding the sellers.

Think about what that means. The companies spending hundreds of billions on AI data centres are seeing their valuations compress, while the companies supplying the memory, chips, and equipment are seeing their valuations soar.

It’s a bifurcated market. AI capex spenders on one side, AI capex beneficiaries on the other.

The Investor’s Dilemma

If you’re sitting on a heavy allocation to the Magnificent Seven right now, you’re facing a genuine dilemma.

Selling them to buy into Micron, SanDisk, and semiconductor stocks feels like chasing a runaway train. These stocks are already up hundreds of percent. The risk of being the last buyer is real.

But staying put feels punishing too, watching your portfolio drift sideways or lower while AI infrastructure stocks surge higher week after week.

Here’s how I think about it.

If you’re a short-term momentum trader, go with the leaders. The AI beneficiaries, memory makers, chip equipment companies, data centre infrastructure plays, have the momentum. Follow it, but have your sell rules ready. These things can reverse as fast as they run.

If you’re a long-term investor, don’t abandon your long-term winners for short-term excitement. Microsoft, Alphabet and Amazon are still building the AI era’s critical infrastructure. Their capex today is an investment in their competitive moat tomorrow. Yes, the market is punishing them now for spending. But those who stay patient may be rewarded when that spending translates into earnings.

The worst thing you can do is panic out of quality compounders at a cyclical low point, only to chase the hot momentum trade at the peak.

Just as we thought AI stocks had run too far, Micron delivered a quarter that made new highs look cheap. That’s the thing about momentum. It doesn’t care about your valuations, your gut feeling, or when you think it should stop.

The AI party is far from over. But make sure you know which kind of investor you are before you decide what to do.