Howard Hughes: The Modern Berkshire Hathaway?

Many investors admire Warren Buffett, including even highly successful billionaire hedge fund managers like Bill Ackman. Recently, Ackman announced his vision to transform one of his portfolio companies, Howard Hughes, into a modern-day Berkshire Hathaway. Here’s what he said on X:

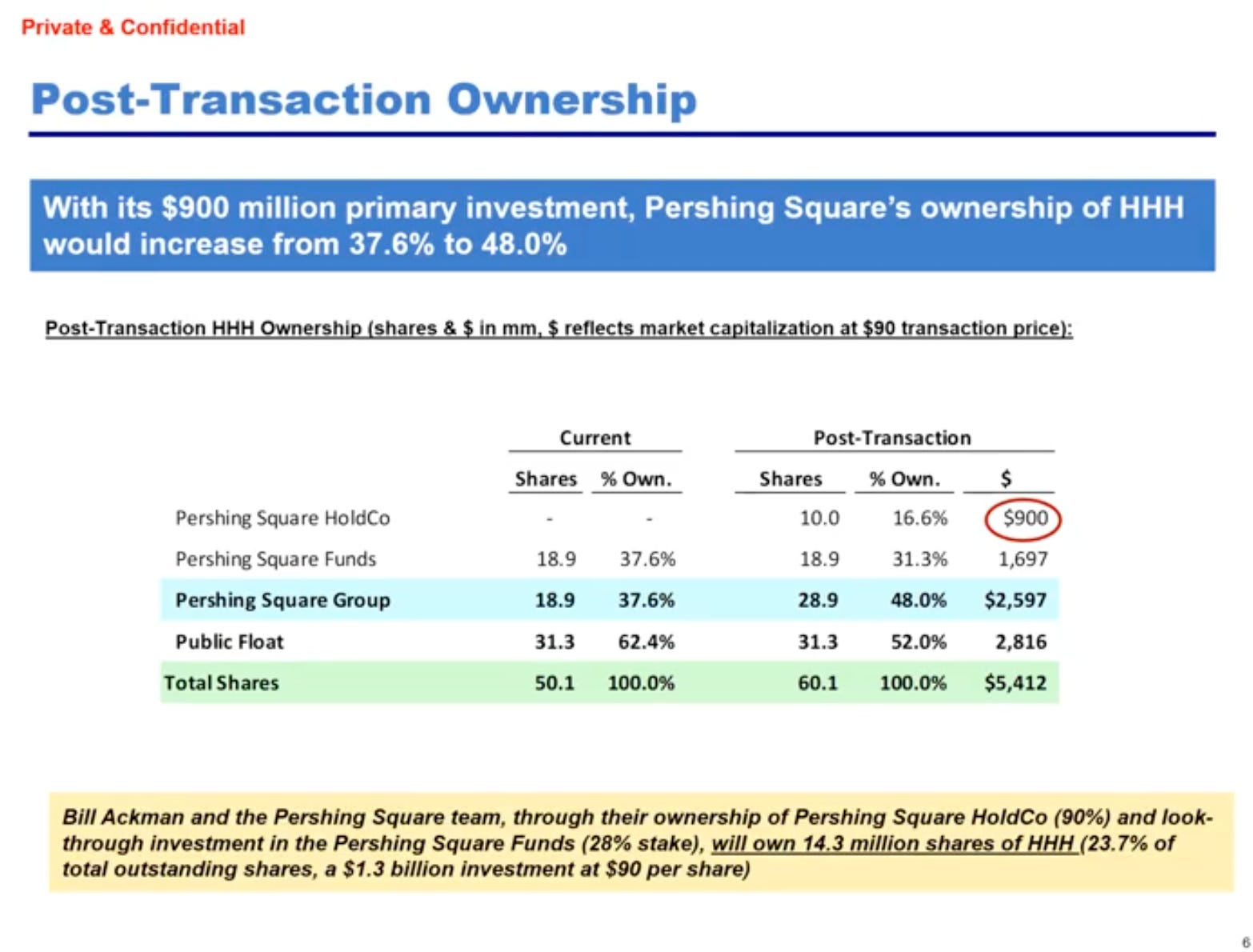

The deal involves Pershing Square HoldCo, a separate entity from Pershing Square’s fund business, owned by Bill Ackman and his colleagues, purchasing $900 million worth of Howard Hughes Holdings (HHH) shares at $90 per share. These will be newly issued shares, meaning the $900 million will go directly into HHH, providing capital for future acquisitions. If completed, Pershing Square’s stake in HHH will increase to 48%.

Bill Ackman will take on the roles of Chairman and CEO of HHH. The key change is that the Pershing Square team will now oversee investment decisions for HHH, focusing on acquiring profitable and growing businesses—much like how Warren Buffett selects companies for Berkshire Hathaway. This is what Ackman means by turning HHH into a modern-day Berkshire.

HHH will remain publicly listed, and Pershing Square has committed not to withdraw capital or sell down its stake, signaling a long-term commitment to making HHH a successful and valuable investment.

Unlike other corporations that form their own investment committees, HHH will instead leverage Pershing Square’s expertise for investment research, idea generation, and deal structuring. In return, HHH will pay Pershing an annual management fee of 1.5%.

This is where some investors have raised concerns about how this differs from Berkshire Hathaway, where Buffett does not charge shareholders a management fee. However, it’s important to recognize that resources need to be compensated, and hiring top-tier investment talent would likely cost more than the 1.5% fee. Ackman pointed out that while Buffett takes a $100,000 annual salary, his deputies, Greg Abel and Ajit Jain, each earn $20 million, while investment managers Ted Weschler and Todd Combs receive $10 million each, plus profit-sharing if their returns outperform the S&P 500. So, Berkshire isn’t as low-cost as many assume.

In my view, the 1.5% annual fee is reasonable and well below market rates compared to private equity firms like KKR and Apollo, which often charge both management and performance fees. Even Pershing Square Holdings (PSH), the London-listed closed-end fund, pays a 1.5% management fee plus a 16-20% performance fee. By comparison, the service fee to HHH is quite fair. At the end of the day, investors care more about performance than quibbling over fees.

Ackman has proven that he is worth the fees. He is one of the best-performing hedge fund managers, with a track record spanning over 20 years. His fund has delivered a 2,388% total return (24% annualized), far surpassing the S&P 500’s 718% return (14% annualized). Without a performance fee, the returns would have been even higher—4,451% total (27% annualized). Investors wouldn’t mind paying the fees for such exceptional performance.