Berkshire Up 16%, S&P Down 5%—The Case for Value Investing in 2025

We’ve been talking about sector rotation in recent posts—quasi-staples, international value, consumer staples, and the like. Another group of stocks investors may want to consider—if you believe this rotation will continue—is U.S. Large Cap Value.

Value stocks have remained relatively undervalued compared to their growth counterparts. But in the recent market selloff, value stocks have actually held up better.

As shown in the chart below, small-cap value stocks are currently the cheapest group. However, they tend to be less defensive, as these smaller companies may lack the financial strength to weather an economic slowdown as effectively as their large-cap peers. So sticking with large cap value will be a more prudent move.

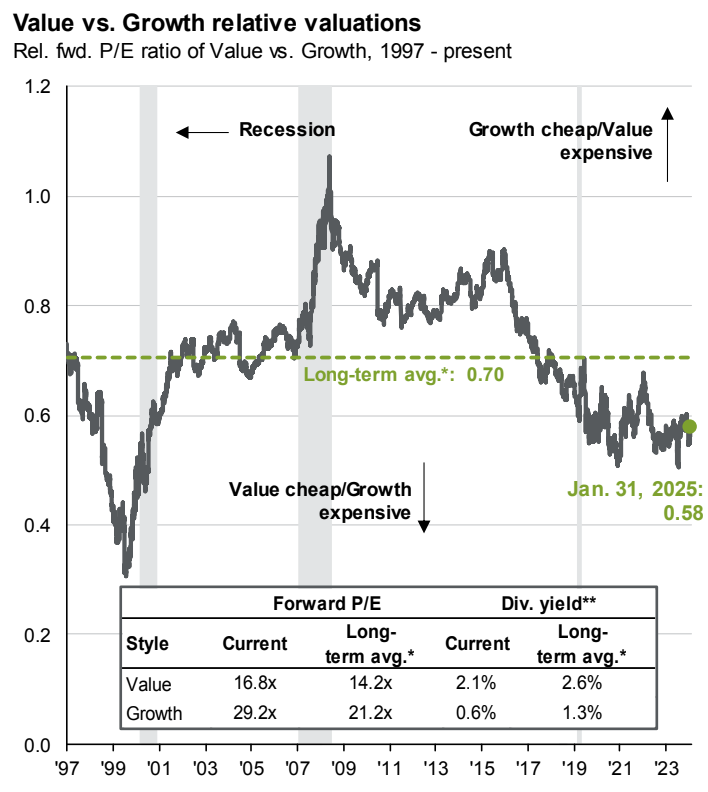

There’s been a prevailing belief that "value is dead" over the past few years (just look at the JPMorgan chart below—value has been cheaper than growth since 2017!). But that narrative could be changing. With interest rates staying higher for longer and economic growth slowing, the environment looks less favorable for growth stocks—and more supportive of a value comeback.

Let’s look at some numbers. Year-to-date, the S&P 500 is down 5%, while the Vanguard Value ETF (VTV) is holding up with a nearly 1% gain. Berkshire Hathaway, known for its value-oriented investments in wide-moat companies, is up 16%.

Now, to be fair, not every stock in Berkshire’s portfolio is a textbook value play. Take Apple—some would argue it’s a growth stock, and it’s Berkshire’s largest holding. But Morningstar classifies it as a value stock, and with its current single-digit annual growth rate, it’s not the high-growth story it used to be. Overall, most of Berkshire’s holdings are slow-growth businesses, so we can reasonably say the portfolio has a value tilt.

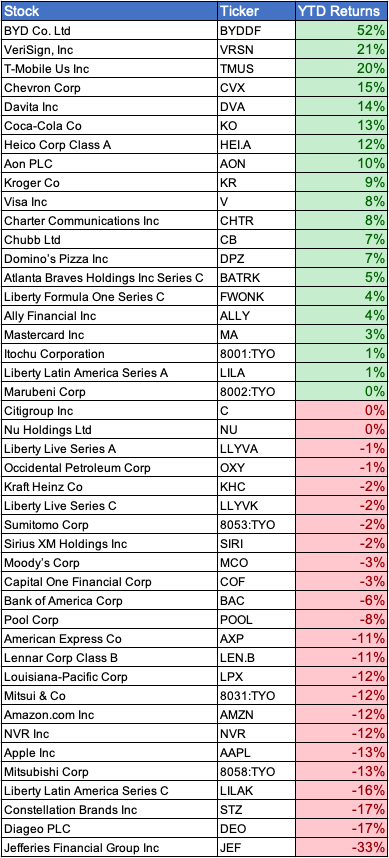

We tallied Berkshire’s portfolio performance year-to-date. On average, the stocks are up around 8%, but when weighted by size, the return actually drops to -1.5%! So how did Berkshire Hathaway’s own stock rise 16%?

We believe there are three key reasons:

Private assets – Berkshire owns several private businesses, including Berkshire Hathaway Energy, and energy stocks have done well.

Cash – Berkshire has a massive cash pile of $334 billion! Investors see this as a source of dry powder that could be deployed smartly when valuations get more attractive.

Flight to safety – In uncertain times, investors gravitate toward stability. Berkshire is seen as a relatively low-risk, dependable investment—especially compared to speculative or high-growth names.

All that said, Berkshire Hathaway remains a solid proxy for value exposure, alongside VTV, for investors who prefer not to pick individual stocks.

In the U.S., concerns are growing about an economic slowdown and consumption downgrade. Avoiding consumption-dependent stocks is one way to reduce risk—names like American Express, Visa, and Mastercard could feel the pinch. Meanwhile, energy, telecom, and healthcare are likely to prove more resilient.

We believe it's time to increase exposure to value and play a bit more defense. Even if growth stocks still make up the bulk of your portfolio, it doesn’t hurt to have some value exposure—especially if the growth slump persists.