Avoid Consumer Discretionary Stocks—Buy These Quasi-Staples Instead

We believe the theme of consumer downgrade is playing out across markets. What was once mainly a China problem—where sluggish consumption followed the collapse of the property bubble and hurt many luxury brands reliant on Chinese spending—is now showing up in the U.S. as well. This is more critical because the U.S. economy is heavily driven by consumption, and any slowdown will have significant ripple effects.

As such, we think most consumer discretionary stocks still have more downside and may not be attractive buys at this point. If one wants exposure, it may be wiser to look for established brands that behave more like consumer staples—businesses people turn to even in tougher times.

Take Lululemon, the latest casualty. Its stock tanked 10% after releasing its results. While 4Q 2024 revenue grew 13%, its 2025 guidance disappointed with a projected 5%–7% growth. That’s a clear signal that this may not be a strong year for consumer spending.

Nike looks worse—it’s expecting a mid-single-digit decline in revenue. The stock has already been slumping and is down another 11% this year.

Deckers, a rising competitor with its popular Hoka brand, also saw its rally reverse—down 43% this year, despite still guiding for 15% growth in 2025. The market seems to be taking a cautious stance on consumer brands, regardless of growth.

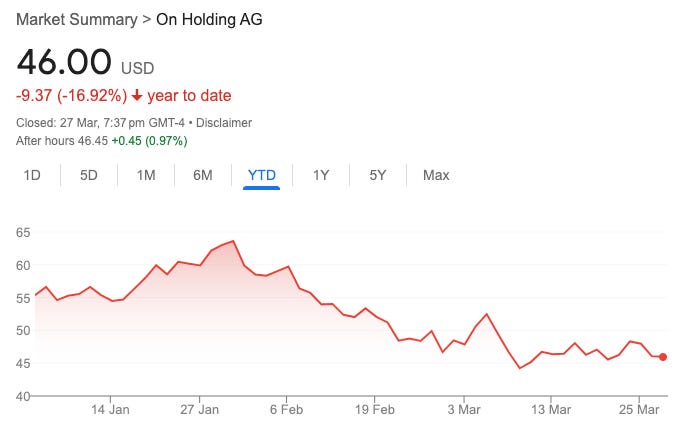

On Running (ON), another fan favorite in the performance footwear space, is forecasting a robust 28% revenue growth in 2025. Even so, the stock is down 17% this year. That tells us the market is risk-off and unwilling to pay up for growth in consumer discretionary right now.

And it's not just about shoes and apparel. In the Quick Service Restaurant (QSR) space, younger chains have also taken a hit, while incumbents have made gains.

Chipotle, Wingstop, and CAVA are down more than 15%, while old guards like McDonald’s (MCD) and Yum! Brands (YUM) are in the green. Investors seem to be rotating away from high-growth names toward defensive plays—reversing the trend of the past few years.

Domino’s (DPZ) is up 12% this year. Even Buffett saw value in picking it up. While technically consumer discretionary, we’d argue that MCD, YUM, and DPZ behave more like staples. These are everyday brands people are unlikely to cut even in a recession. That makes them the rare bright spots where opportunities may exist.

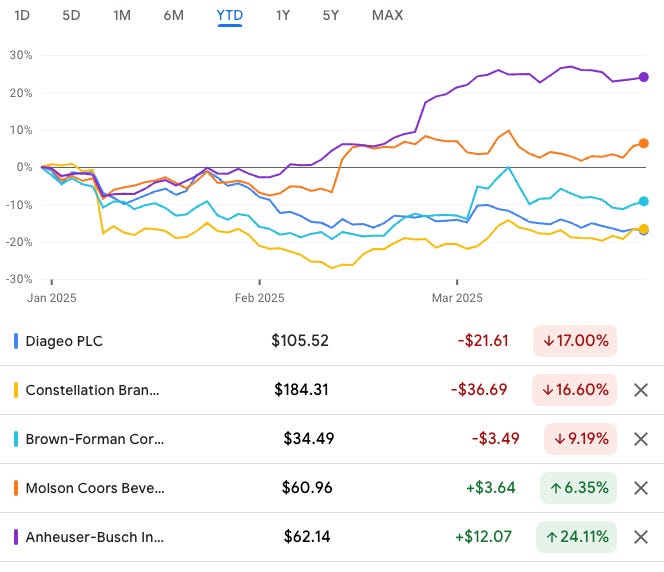

Alcohol is another interesting subsegment. Buffett bought Constellation Brands (STZ) after its stock has struggled, as have Diageo and Brown-Forman. Yet Molson Coors (TAP) and Anheuser-Busch (BUD) are holding up with modest gains. This may reflect how beer—being cheaper and more widely consumed—behaves more like a staple, while spirits are more elastic in tough times.

There’s also a tariff angle—TAP and BUD produce mostly in the U.S. and are less affected by cross-border tariffs. In contrast, STZ gets 85% of sales from Mexican beer, making it more vulnerable to geopolitical risk.

Lastly, one new group worth highlighting is automotive parts suppliers. With tariffs raising the cost of new cars and a weaker economy encouraging people to hang on to their existing vehicles, demand for repairs and parts has surged. These stocks have quietly done well this year, emerging as another category of quasi-staples within the discretionary sector.

Below is a list of quasi-staple stocks that we believe deserve closer attention within the consumer discretionary sector—names that exhibit defensive qualities and may offer more resilient opportunities in a slowing economy.