7 Big Earnings Moves

What a day of action! The US market opened strongly but eventually closed down. I noticed several stocks experiencing significant moves following the release of their quarterly results. These movements certainly caught my attention, and I believe you might be interested too. The crucial question is: among these stocks, which ones do I consider worth investing in?

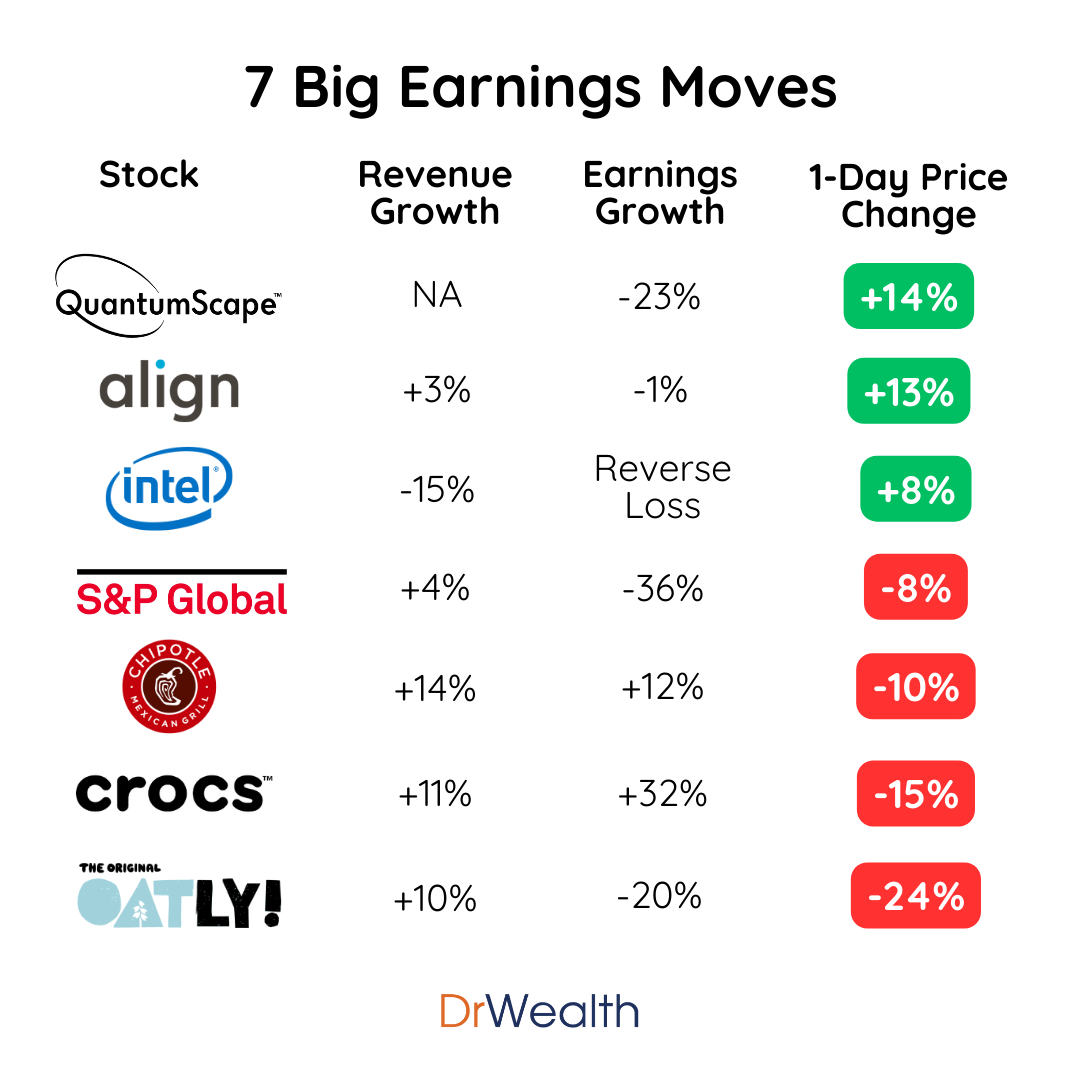

Quantumscape (QS) +14%: A Speculative Opportunity

The share price of a solid-state EV battery manufacturer surged by an impressive 42% at one point during the day before settling for a 14% gain at closing. This price movement was not triggered by its larger loss reported in the second quarter.

Instead, it is due to its collaboration with an automaker to introduce its inaugural product, the QSE-5, to the market. This represents a significant achievement for a company that currently lacks any commercialized products or revenue. There is potential for further growth if the product indeed hits the market with the backing of a major brand. However, it's essential to note that this investment is speculative at best and not suitable for long-term strategies.

Align Tech (SLGN) +13%: Fairly Valued

The owner of Invisalign surpassed analysts' expectations for both revenue and earnings. Additionally, they raised the revenue guidance for the next quarter by 12%. It appears that Align Tech is making a turnaround, recovering from the impact of lockdowns in the Chinese market last year and overcoming forex losses due to a strong USD. Their share price has surged by an impressive 82% year-to-date, and currently, it is hovering around fair value and not much margin of safety to buy at the moment.

Intel (INTC) +8%: Still On A Decline = Avoid

Intel has lost its edge to chip designers like AMD and Nvidia as well as foundries such as TSMC and Samsung. As fewer investors are rooting for Intel, a rosier set of results would lift sentiments easily. Intel managed to achieve a profit despite analysts predicting a loss.

While its revenue exceeded estimates, it still declined compared to the previous year, marking the sixth consecutive quarter of falling sales. The company's earnings were bolstered by cost-cutting measures rather than revenue growth, indicating that Intel's challenges are not fully resolved. There is a limit to how much cost can be cut, so the road ahead remains uncertain for the company.